AI adoption has surged in companies of all sizes, and ISO 42001 has become the standard way to measure AI governance. Latest data reveals that 72% of organizations use AI in at least one business function, a sharp increase from 55% the previous year. This growth stands out in the fintech sector where companies handle sensitive and regulated data regularly.

The regulatory landscape keeps evolving. The EU AI Act came into effect on August 1, 2024, and will apply fully by August 2, 2026. As a result, 76% of organizations plan to align with AI compliance frameworks like ISO 42001 soon. Many fintech firms either need this compliance now or will need it shortly.

This piece explains why fintech AI operations must get ISO 42001 certification. You’ll learn practical ways to build an AI Management System (AIMS) and achieve audit-ready compliance while integrating ISO 42001 requirements with current frameworks. Companies with ISO 27001 certification can get ISO 42001 compliance 40% faster than others starting fresh. This advantage matters a lot in today’s ever-changing regulatory world.

Operationalizing ISO 42001 for Fintech AI Governance

ISO 42001 implementation needs a well-laid-out approach that deals with fintech’s unique AI governance challenges. Organizations must know their role in the AI ecosystem—whether as a provider, producer, or user. This knowledge helps define the scope of their compliance efforts.

Building an AI Management System (AIMS) for fintech

A complete AI Management System that follows the Plan-Do-Check-Act cycle forms the foundation of ISO 42001 compliance. Fintech companies need governance structures that arrange AI systems with regulatory standards. These structures manage industry-specific risks like algorithmic bias in credit decisions or transaction monitoring. The AIMS framework must have:

- Risk management protocols that identify and reduce AI-related vulnerabilities

- Policies that govern model development, deployment, and monitoring

- Compliance mechanisms that meet both ISO 42001 and financial regulatory requirements

A well-designed AIMS helps fintech organizations show their early adopter status. This enhances stakeholder trust and sets them apart from competitors.

Assigning ownership and accountability for AI systems

Board members must actively oversee AI technology as its use grows. ISO 42001 demands clear ownership at the highest levels. Top management must show leadership and dedication to the AIMS. This involves:

Clear accountability mapping that defines responsibilities among developers, business leaders, and users. Fintech organizations with existing ISO 27001 certification can create a unified governance structure. This structure covers both information security and AI risk management when they integrate ISO 42001.

Aligning ISO 42001 clauses with fintech risk categories

Fintech AI systems face unique risks that ISO 42001 controls must address. Organizations should map AI risks found during threat assessment to matching ISO 42001 clauses and Annex A controls. Fintech companies should focus their implementation on:

Cybersecurity risks from prompt injection and collateral training damage Regulatory compliance with financial services requirements Ethical implications of automated financial decisions

This risk-based approach ensures fintech organizations apply ISO 42001 controls based on each AI system’s potential harm.

Audit-Ready Compliance Under Article 113 and ISO 42001

Image Source: Vanta

Getting ready for ISO 42001 audits needs a step-by-step approach. This turns abstract compliance rules into clear, verifiable evidence. Companies should focus on operational proof that regulators can verify instead of just having paperwork.

Mapping ISO 42001 controls to EU AI Act enforcement phases

The EU AI Act implementation uses a step-by-step approach through Article 113. Different rules become active at specific dates. ISO 42001 gives a well-laid-out framework that lines up with these enforcement phases. Fintech companies can benefit from linking ISO 42001 clauses directly to Article 113’s requirements. This connection:

- Risk-appropriate controls: Groups AI systems by risk level as the EU AI Act requires

- Unified compliance timeline: Matches ISO 42001 setup with Article 113 deadlines

- Defensible governance: Shows responsible AI management through trusted international standards

Checklist-driven compliance with timestamped artifacts

ISO 42001 compliance has moved beyond basic paperwork to focus on proof you can verify. Each part of compliance needs:

- People who own and take charge of specific controls

- Time-stamped proof that shows real action, not just plans

- Evidence that connects each rule to its supporting documents

Fintech firms must keep detailed records of bias testing, oversight actions, and how they handle incidents. These records need exact timestamps and clear ownership. This documentation protects you during audits by proving your controls work in practice.

Real-time dashboards for audit visibility

Old-school audit prep often meant rushing to gather documents. But ISO 42001 compliance works better with up-to-the-minute data analysis through dashboards. These tools:

- Show how well you meet all ISO 42001 controls

- Catch overdue reviews and missing evidence before they cause problems

- Let auditors check controls directly through secure, role-based access

The work to be done means closing the gap between daily operations and what regulators need. Good mapping, solid proof, and constant monitoring help fintech companies turn ISO 42001 from a box-ticking exercise into a real advantage. This builds trust with regulators, partners, and customers alike.

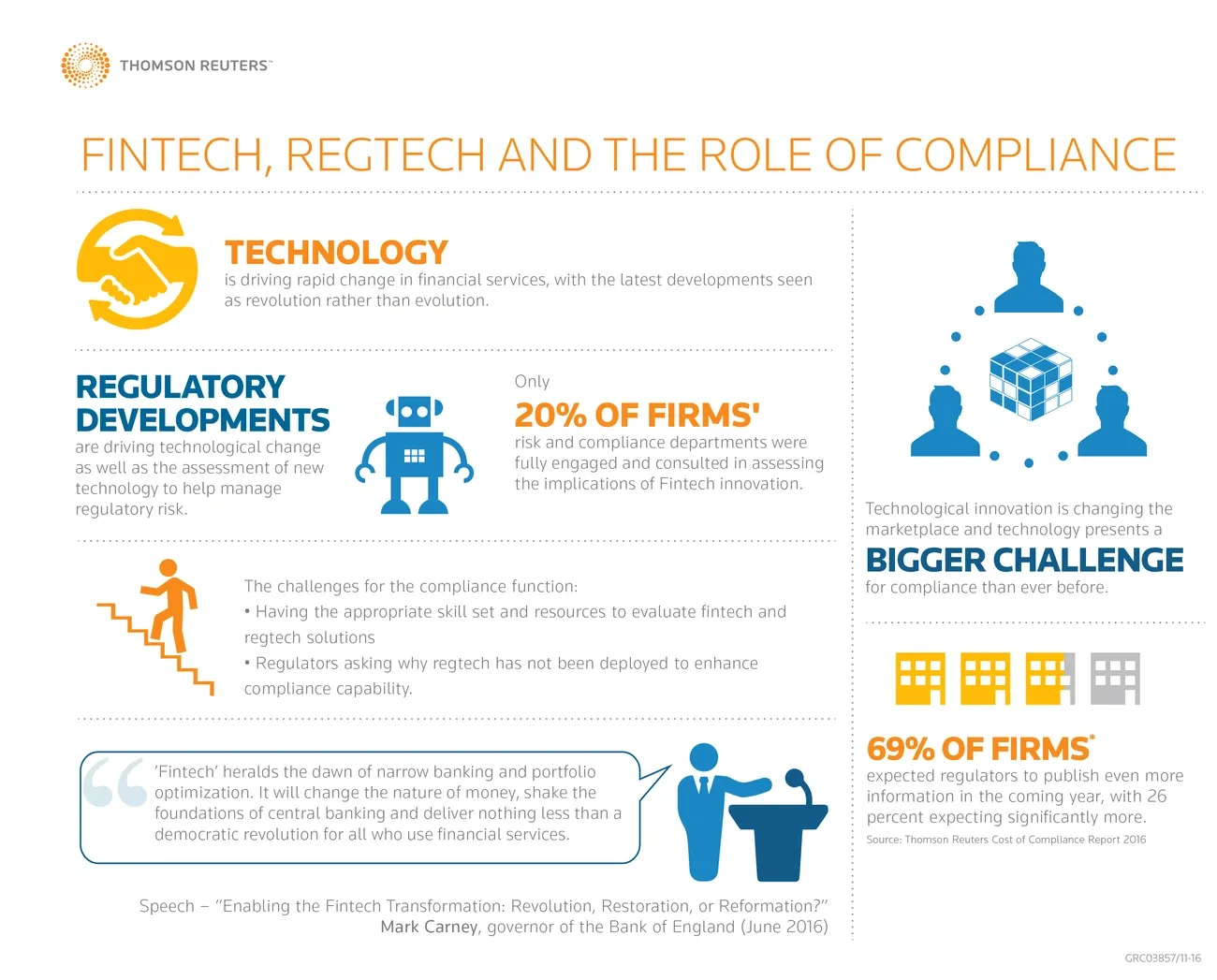

Benefits of Early ISO 42001 Adoption for Fintech Firms

Image Source: Thomson Reuters Legal Solutions

Smart fintech companies know that waiting to deal with AI risks until they become regulatory requirements isn’t a good strategy. Companies that adopt ISO 42001 early gain strategic advantages beyond basic compliance.

Reducing regulatory and reputational risk

Recent data reveals that 38% of organizations consider regulatory compliance their biggest obstacle to AI deployment. This worry makes sense, since EU AI Act violations could lead to penalties up to €35 million or 7% of global turnover. Several jurisdictions now recognize ISO 42001 as a potential safe harbor that proves responsible AI governance, as shown in the Colorado AI Act.

Improving stakeholder trust and market positioning

UK financial leaders’ concerns about AI-related compliance exceed 60%. ISO 42001 certification offers a proven way to show ethical and responsible AI use. This difference becomes a key advantage when companies:

- Pursue new business deals

- Attract top talent

- Seek funding from outside investors

Companies that use governance as a trust signal see faster customer adoption and less friction in their sales cycles.

Avoiding last-minute compliance costs and delays

Companies that adopt ISO 42001 early avoid higher costs related to:

- Noncompliance fines

- Missed market opportunities

- Rushed implementations

- Governance gaps

Proactive certification turns compliance from a simple checkbox into a strategic asset that builds market confidence and reduces long-term regulatory exposure.

Integrating ISO 42001 with Existing Fintech Compliance Frameworks

Image Source: Binmile

Fintech organizations often need to follow multiple compliance frameworks at once. ISO 42001 makes this easier because it was built to work well with other standards, which helps companies manage overlapping requirements more efficiently.

ISO 42001 and ISO 27001 dual certification strategy

ISO 42001 shares the same Annex SL structure as ISO 27001. Companies that already have ISO 27001 certification match about 60-70% of ISO 42001 requirements. This makes it possible to get both certifications by expanding their current system to include AI-specific controls. Companies with ISO 27001 certification can get ISO 42001 compliance 40% faster than those starting fresh.

The main difference lies in what each standard covers. ISO 27001 protects information security for all assets, while ISO 42001 focuses on AI-related concerns like ethics, bias reduction, and explainability.

Complementing GDPR, PCI DSS, and SOC 2 with ISO 42001

ISO 42001 works naturally with existing frameworks instead of replacing them. Companies using SOC 2 or HITRUST can add ISO 42001 to boost their control environment with AI lifecycle and transparency requirements. ISO 27001 already fits well with over 20 global regulations including GDPR and PCI DSS, which creates a strong base for unified compliance.

This smart arrangement helps strengthen data protection while making sure AI systems handle both customer privacy and payment security properly.

Using GRC platforms to manage overlapping controls

Companies can get tired of managing multiple standards. GRC (Governance, Risk, and Compliance) platforms give fintech firms a single system to handle controls, risks, and audit evidence. These platforms:

- Unite controls, risks, and policies in one auditable environment

- Show live dashboards of risk and control status

- Tag each risk, control, and evidence artifact with its parent standard and clause

Success depends on being precise because shortcuts lead to failed audits and missed ground risks.

Conclusion

Fintech companies are under immense pressure to adopt ISO 42001 as AI becomes deeply woven into financial services. The EU AI Act’s regulatory demands and market pressures make compliance unavoidable. Companies that take the lead in implementing ISO 42001 end up with major advantages beyond just meeting regulations.

A well-laid-out approach to building an AI Management System gives fintech firms solid governance frameworks that tackle their industry’s unique risks. The system maps clear accountability and uses risk-based implementation to keep AI systems compliant and ethical. On top of that, it turns abstract requirements into solid proof through timestamped records and live dashboards.

Companies that adopt ISO 42001 early definitely see less regulatory risk, stronger stakeholder trust, and stand out in the market. This standard works both as a compliance tool and a strategic asset that builds trust with customers, investors, and partners.

ISO 27001-certified fintech organizations have the biggest advantage. They can achieve ISO 42001 compliance up to 40% faster because the standards share similar structures. This efficiency carries over to other frameworks like GDPR and SOC 2, creating one unified approach that covers both information security and AI-specific needs.

Moving forward needs careful planning and execution. Companies should check how well they match ISO 42001’s requirements and create an implementation plan. Fintech leaders ready to start should Book a Readiness Call to assess their needs and find ways to streamline certification.

ISO 42001 is more than just another box to check – it offers a detailed framework to develop and deploy AI responsibly. Financial technology firms that adopt this standard now are at the vanguard of trustworthy innovation, avoiding the rush to comply as regulatory deadlines get closer.

Key Takeaways

ISO 42001 compliance is rapidly becoming essential for fintech companies as AI adoption accelerates and regulatory frameworks like the EU AI Act take effect. Here are the critical insights every fintech leader should understand:

• Early adoption provides competitive advantage: Organizations with existing ISO 27001 certification can achieve ISO 42001 compliance up to 40% faster, transforming regulatory requirements into market differentiation.

• Structured governance prevents costly scrambles: Building an AI Management System (AIMS) with clear accountability mapping and risk-based controls helps avoid last-minute compliance costs and potential fines up to €35 million.

• Integration amplifies existing frameworks: ISO 42001 complements GDPR, PCI DSS, and SOC 2 without duplication, creating unified governance that addresses both data security and AI-specific risks.

• Audit-ready compliance requires verifiable evidence: Success depends on timestamped artifacts, real-time dashboards, and continuous monitoring rather than static documentation that fails under regulatory scrutiny.

• Regulatory pressure is intensifying rapidly: With 76% of organizations planning AI compliance initiatives and the EU AI Act fully applicable by August 2026, proactive certification becomes a strategic necessity rather than optional consideration.

The window for strategic ISO 42001 implementation is narrowing as regulatory deadlines approach. Fintech companies that act now can transform compliance from a burden into a competitive asset that builds stakeholder trust and market positioning.

FAQs

Q1. What is ISO 42001 and why is it important for fintech companies? ISO 42001 is a standard for AI governance that is becoming crucial for fintech companies. It provides a framework for managing AI-related risks, ensuring ethical AI use, and demonstrating compliance with regulations like the EU AI Act.

Q2. How can fintech firms benefit from early adoption of ISO 42001? Early adoption of ISO 42001 can help fintech firms reduce regulatory and reputational risks, improve stakeholder trust, gain a competitive advantage in the market, and avoid last-minute compliance costs and delays.

Q3. How does ISO 42001 integrate with existing compliance frameworks? ISO 42001 complements existing frameworks like ISO 27001, GDPR, PCI DSS, and SOC 2. Organizations with ISO 27001 certification can achieve ISO 42001 compliance up to 40% faster due to structural similarities between the standards.

Q4. What is an AI Management System (AIMS) and why is it important? An AI Management System (AIMS) is a comprehensive framework for governing AI operations. It’s crucial for fintech companies to establish an AIMS to ensure AI systems align with regulatory standards and manage industry-specific risks like algorithmic bias.

Q5. How can fintech companies prepare for ISO 42001 audits? To prepare for ISO 42001 audits, fintech companies should map ISO 42001 controls to EU AI Act enforcement phases, implement checklist-driven compliance with timestamped artifacts, and use real-time dashboards for continuous monitoring and audit visibility.