Financial sector spending on AI governance is projected to jump from $35 billion in 2023 to $97 billion by 2027. AI has evolved from an innovative technology to become a vital part of modern financial services. Banks and financial institutions now use AI to power fraud detection systems that spot unusual patterns in massive transaction volumes and run automated trading platforms that make decisions based on up-to-the-minute market data.

The quick adoption of AI brings major regulatory hurdles. AI-powered compliance tools could save the financial industry over $1.2 billion each year by 2025. Yet poor model risk management can lead to regulatory fines, expensive fixes, and lost trust from regulators. The rules of the game have changed for good, and regulators worldwide have made it clear – AI systems must follow the same consumer protection laws as traditional systems.

This piece outlines six proven strategies to build effective AI governance frameworks and model risk management practices. These strategies can help organizations dodge expensive penalties while getting the most from AI technology. Financial institutions should remember that despite AI’s huge potential in banking, they stay responsible for following regulations, even when using outside models.

Understanding AI Governance in FinTech Context

Image Source: Holistic AI

“The emergence of AI is disrupting the physics of the industry, weakening the bonds that have held together the components of the traditional financial institutions, and opening the door to more innovations and new operating models.” — Deloitte, Global business research and consulting firm specializing in financial services and AI impact analysis

Traditional AI systems in finance used to focus on narrow tasks with proprietary business data. Generative AI has altered the map by creating new content through complex, multistep processes. This brings new opportunities for misuse and error. Financial institutions need to rethink their ai governance with frameworks built for this new reality.

Defining AI Governance Framework in Financial Services

The ai governance framework in financial services is a well-laid-out system of policies, standards, and processes. It guides the entire lifecycle of AI systems. The main goal is to maximize benefits while reducing major risks like bias and privacy violations. This helps ensure compliance with changing regulations, builds public trust, and promotes innovation.

These four core components make an ai governance framework work:

- Definitions: Common language about AI models and systems makes interagency collaboration easier

- Inventory: Tracking AI/ML systems and their associated risks

- Policies/Standards: Detailed guidelines for data handling, algorithm transparency, and user consent

- Controls: Monitoring, validation, and governance mechanisms

Financial institutions start with centralized organizational models for AI risk management. They gradually move toward partially or fully decentralized models as their capabilities grow. This development helps balance innovation with proper oversight as the organization’s ai data governance practices become more refined.

Why FinTechs Face Unique AI Compliance Pressures

Fintech companies deal with unique AI challenges that traditional financial institutions might not face. About 55% of organizations haven’t set up an AI governance framework. This creates both risks and competitive opportunities.

Fintech companies get extra scrutiny because their AI applications directly affect critical regulated activities:

- Customer-facing applications: Chatbots and AI tools need special oversight to comply with consumer protection laws

- Credit scoring and underwriting: AI algorithms must avoid bias or discrimination

- Fraud detection systems: Models need to balance accuracy with fairness across protected classes

Fintech companies work across multiple jurisdictions with different rules. The EU AI Act groups AI systems by risk levels. High-risk systems like credit scoring tools need thorough testing and reporting. The United States doesn’t have one main AI law. It relies on guidance from agencies like the Federal Reserve, OCC, and CFPB.

Fintechs must guide through this complex regulatory landscape while staying innovative. This creates unique pressures that need specialized ai governance consulting approaches for their business model.

AI Governance vs Traditional Risk Controls

Traditional AI-risk-governance systems can’t handle the complexity of advanced AI technologies. The biggest difference lies in how newer AI models work compared to traditional systems.

Traditional models handle specific tasks with structured data. Newer fintech ai use cases use multitasking models to create personalized services, boost customer engagement, and optimize operations. These benefits come with their own risks:

- Increased complexity: Generative AI models blend different models and components. They need specialized oversight beyond a single risk committee

- Expanded data sources: Models trained on public and private data might produce wrong or made-up information

- Intellectual property concerns: AI tools could expose proprietary algorithms or suggest code with licensing issues

Financial institutions must update their ai model risk management approaches. They can’t rely on one group to oversee all AI applications. They need to decide which AI components need model risk review alone versus joint review with other risk committees.

Effective ai risk management banking means building governance into organizational structures that line up with business goals. AI isn’t just a technological consideration. This approach creates ai governance contextual organizational truth – governance that fits the organization’s real needs and operations.

Use Cases That Trigger Regulatory Scrutiny

Image Source: LeewayHertz

Financial regulators pay extra attention to specific fintech ai use cases that could affect consumer welfare and financial stability. Regulators worldwide watch AI applications in high-risk scenarios closely. Their enforcement actions show clear patterns they worry about.

AI-Powered Credit Scoring and Underwriting

AI adoption in credit decisions has drawn regulatory scrutiny about fairness and transparency. Banks using AI-based credit scoring systems face strict reviews under frameworks like the Equal Credit Opportunity Act (ECOA). Regulators worldwide have made it clear that “the algorithm decided” no longer works as a legal defense for credit denials.

Wells Fargo faced discrimination charges in 2022. Investigations showed their algorithm gave Black and Latino applicants higher risk scores than white applicants with similar finances. A similar case emerged in 2025 when Massachusetts authorities settled with Earnest Operations LLC for $2.50 million. Their AI models broke consumer protection laws by embedding bias in lending decisions.

The Consumer Financial Protection Bureau (CFPB) doesn’t accept generic adverse action notices or checklists from creditors. Lenders must give specific, behavioral reasons for credit denials, even if these reasons might upset consumers. A simple reason like “purchasing history” won’t work. Instead, lenders need details such as “multiple cash advances exceeding 30% of income in past 60 days”.

Fraud Detection and AML with Machine Learning

Banks spend about $214 billion yearly on financial crime compliance. Machine learning plays a central role in these efforts. While machine learning makes anti-money laundering (AML) better, these systems face intense regulatory oversight.

Machine learning models work better at transaction monitoring. One major bank reported 40% better suspicious activity detection and 30% more efficiency after switching from rule-based tools to AI models. Yet these improvements bring new regulatory challenges about model explainability and validation.

Banking regulators expect solid model risk management practices for AI-powered fraud detection. Banks must show three elements in their AI compliance:

- Out-of-time sample testing with sufficient reserves

- Detailed model validation that tackles ML-specific risks

- Regular below-the-line (BTL) monitoring of model performance

Regulators look beyond technical performance. They check how banks connect stakeholders, plan safe technology transitions, and strengthen model risk management.

Chatbots and Customer-Facing AI Tools

AI chatbots and virtual assistants worry regulators more each day. About 37% of Americans used bank chatbots in 2022. This number could reach 110.9 million users by 2026. Every top 10 commercial bank in America now uses chatbots of different complexity.

The Federal Trade Commission has started looking into AI chatbot providers. They want to know how these companies “measure, test, and monitor potentially negative impacts” of their technology. Regulators worry about:

- Inappropriate disclosures: California’s BOTS Act says companies must tell users when they talk to automated bots in certain cases

- “Doom loops”: Users get stuck in endless cycles of unhelpful responses without human help

- Security vulnerabilities: Users might share too much information through chatbot interfaces

Chatbots must follow all federal consumer financial laws, even for simple customer service. Banks could face penalties if they break these standards. Banks need strong ai governance frameworks that handle these specific cases to reduce regulatory risks.

Proven Way #1: Build a Contextual AI Governance Framework

Creating a useful ai governance framework needs more than basic approaches. Your organization needs a system that matches its business needs and daily operations. A good framework tackles specific risks and enables breakthroughs without putting up unnecessary barriers. A well-laid-out framework helps you avoid weak controls while preventing excessive rules that hold back tech progress.

Making AI Governance Work for Your Business

AI governance works best when it connects directly to your company’s goals. Many financial firms don’t deal very well with AI because they see it as just a tech project separate from their business strategy. Successful companies make sure their AI projects boost their business goals instead of running separately.

Here’s how to line up your goals:

- Identify your AI purpose – Define AI’s role in your company and how it helps your business model. A clear vision helps save resources as everyone understands how technology should grow.

- Establish oversight mechanisms – Set up or use existing oversight teams to guide AI from the top. This unified approach makes consistent deployment easier across your company and builds confidence in implementation.

- Prioritize use cases strategically – Review potential AI projects based on their business effect and risks. Risk scorecards help you rank fintech ai use cases by business needs and expected returns while spotting issues early.

Companies should avoid letting different departments handle AI their own way. This leads to conflicting priorities and wastes resources. Financial firms that take a planned, top-down approach to ai governance build better foundations for growing AI while keeping proper controls.

Building AI Governance Around Your Organization

“Contextual organizational truth” in ai governance means creating rules that match how your company really works instead of using theoretical ideas that ignore reality. Companies need to blend governance into daily work so following rules becomes natural.

A complete ai governance framework has these connected parts:

- Decision rights and accountability frameworks built into daily work

- Structure and roles with clear AI oversight duties

- Processes that link governance choices to business operations

- Technology enablement tools that support and track governance

Financial firms must decide which AI parts need only model risk checks and which need broader risk committee reviews. This choice should match your company’s risk profile and AI applications.

Your company needs a clear operating model that answers four key questions:

- What business results do we need and why?

- Who makes which decisions?

- When and where do we make decisions, and what depends on them?

- How can tech help manage and track governance?

Your ai governance framework should use existing reliable frameworks for handling tech risk instead of creating new ones. To cite an instance, the FINOS AI Governance Framework suggests creating a monitoring strategy that states clear goals for watching AI systems based on business needs, specific risks, and compliance rules.

Note that contextual ai governance must grow with your organization. As your AI skills improve, your governance will likely change from central control to more distributed models that balance breakthroughs with proper oversight as your ai data governance becomes more advanced.

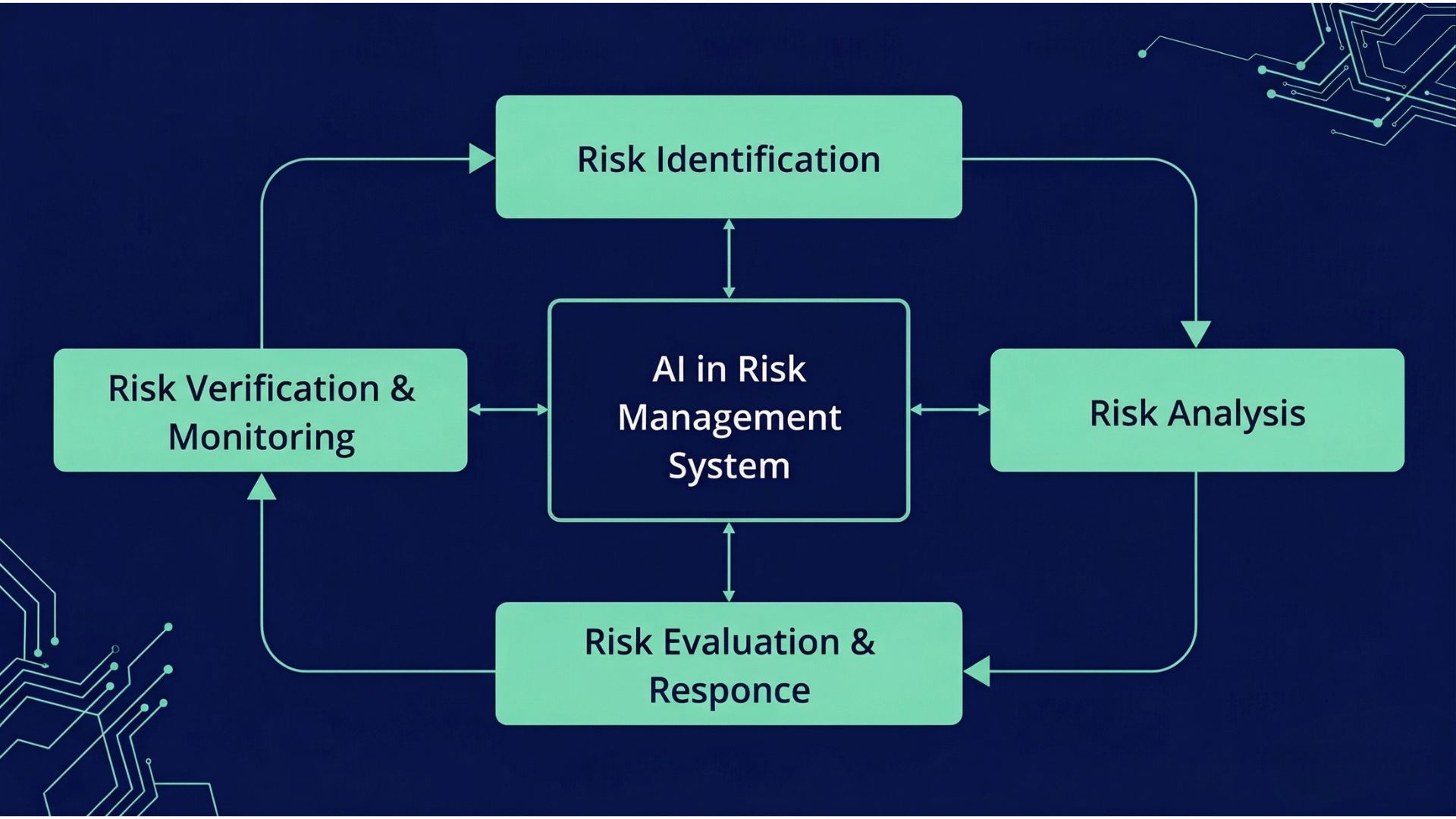

Proven Way #2: Implement Model Risk Management Controls

Image Source: LeewayHertz

Financial institutions need resilient controls to manage ai model risk effectively. These controls verify model performance and minimize potential risks. The life-blood of these controls depends on systematic verification, monitoring, and regulatory compliance. This becomes vital for financial institutions where model failures could result in heavy penalties.

Model Validation and Performance Monitoring

Sound ai governance in financial services relies on model validation. This process confirms that models meet design objectives and business requirements while spotting potential limitations. A detailed validation should look at all model components—inputs, processing, outputs, and reports. This applies to both in-house and vendor-purchased models.

Successful validation demands:

- Independence from model development and use

- Critical review by knowledgeable, objective parties

- Regular periodic reviews (at least annually)

- Evaluation of conceptual soundness and design quality

Performance monitoring plays an equally vital role for AI applications in fintech. Organizations should track key performance indicators like accuracy, precision, recall, and F1 scores. Sudden or gradual decreases might indicate issues that need immediate attention. Organizations must set predetermined thresholds for acceptable performance. Automated alerts should trigger when metrics drop below these levels.

Handling Model Drift and Retraining Cycles

Model drift poses one of the biggest challenges to AI system reliability. Model drift demonstrates itself in several forms:

- Data drift: Changes in input data distribution

- Concept drift: Changes in relationships between variables

- Covariate drift: Common when expanding into new customer segments or markets

Early detection of drift plays a key role in effective ai risk management banking. Industry data shows that monitoring statistical changes in feature distributions helps identify data drift before it affects accuracy. Financial institutions should deploy automated monitoring systems that compare current data distributions with established baselines. These systems use techniques like the Kolmogorov-Smirnov test or Population Stability Index (PSI).

Clear retraining triggers become essential. Models need retraining when drift indicators exceed predetermined thresholds or performance metrics show major degradation. Financial institutions must verify that both data and model pipelines meet expected standards before implementing retrained models. This ensures compliance with ai data governance requirements.

SR 11-7 Compliance for AI Models

The Federal Reserve’s Supervisory Letter SR 11-7 offers a detailed framework for model risk management that directly applies to fintech ai use cases. Compliance requires three core elements:

The first element evaluates conceptual soundness by assessing model design quality and reviewing documentation that supports chosen methods. AI models require explainability testing and robustness checks against adversarial inputs.

The second element involves continuous monitoring to verify appropriate model implementation and performance. AI systems need constant verification to ensure they work within their original scope.

The third element analyzes outcomes by comparing model outputs to actual results through back-testing. AI models in financial services require analysis beyond traditional accuracy metrics to test for bias, fairness, and model drift.

SR 11-7’s application to modern AI systems needs adaptation. Current stakeholders expect institutions to integrate explainability, fairness, transparency, and continuous monitoring into their ai governance frameworks. Deepening their commitment to validation, governance, documentation, and monitoring processes helps meet these expectations and builds long-term resilience.

Proven Way #3: Ensure Explainability and Transparency

“AI is a mirror, reflecting not only our intellect, but our values and fears.” — Ravi Narayanan, VP of Insights and Analytics at Nisum, AI and technology expert

What regulators expect from ai governance has grown beyond just following rules. Financial institutions must now show clearly how their AI systems work. Yes, it is clear from regulators that “a creditor cannot justify noncompliance with ECOA and Regulation B’s requirements based on the mere fact that the technology it employs is too complicated or opaque to understand”.

Using SHAP and LIME for Model Interpretability

SHAP (SHapley Additive exPlanations) and LIME (Local Interpretable Model-agnostic Explanations) are two powerful tools that help explain ai model risk management. These methods form the basis for making models understandable in fintech ai use cases.

SHAP uses game theory principles to give values to each feature and measures their effect on model predictions. This method works for both overall and specific interpretations, making it useful for complex models like credit scoring algorithms. LIME creates local approximations by changing input data and gives an explanation of individual predictions that matter for customer-facing applications.

The key differences between these approaches include:

| Aspect | SHAP | LIME |

| Scope | Global and local interpretability | Primarily local interpretability |

| Stability | More consistent results | May show instability due to random sampling |

| Visualization | Rich set of visualization tools | Focuses on perturbed samples |

| Application | Credit scoring, healthcare predictions | Fraud detection, misclassifications |

These tools help banks explain which factors (income, credit history, debt ratio) affect approvals or rejections. Borrowers can understand their credit ratings while getting valid reasons for decisions.

Generating Specific Adverse Action Notices

Equal Credit Opportunity Act (ECOA) and Fair Credit Reporting Act (FCRA) require financial institutions to give specific, accurate reasons when taking adverse action against consumers. The Consumer Financial Protection Bureau (CFPB) states these notices must show the “principal reason(s) for the adverse action” and must “relate to and accurately describe the factors actually considered”.

Generic adverse action notices are not enough anymore. Your AI models that use alternative data sources or complex algorithms must have notices that:

- Show actual reasons for credit denial, “even if the relationship of that factor to predicting creditworthiness may not be clear to the applicant”

- Give specific details about consumer behavior when relevant (type of establishment, location, or goods purchased)

- Include credit score information when used, with factors that hurt the score

Proper controls around AI models substantially reduce regulatory risks. This includes documenting design choices, testing explanations, and legal review of adverse action notices.

Avoiding the ‘Black Box’ Defense

Regulators have rejected the “black box” defense – saying a model is too complex to explain. The CFPB makes it clear that ECOA and Regulation B do not allow creditors to use “black-box” underwriting technology when it prevents giving specific reasons for adverse actions.

Banks must understand their credit decisioning systems whatever the complexity to meet fair lending obligations. This means they must:

- Use explainable AI frameworks that improve transparency while keeping accuracy

- Get a full picture of AI models before deployment to check “explainability”

- Add human judgment to make AI decisions stronger

Explainability in ai governance is more than just checking a regulatory box – it’s vital for success. It builds trust, increases accountability, and creates a foundation for responsible breakthroughs in financial services. Making use of information through transparent ai data governance helps develop systems that deliver real value while you retain control needed for regulatory compliance.

Proven Way #4: Conduct Regular Bias and Fairness Audits

Bias testing serves as a vital shield against discrimination in AI-powered financial systems. The CFPB mandates that financial institutions must test AI models to prevent bias, disparate treatment, disparate impact, and collateral damage. These rules apply to all AI-based credit decisions, no matter how complex the technology.

Disparate Impact Testing Across Protected Classes

Disparate impact happens when neutral-looking policies hit protected groups harder without a valid business reason. Financial institutions need a well-laid-out testing approach to spot these impacts:

- Run the AI model on a hold-out validation set

- Calculate the selection rate for each protected class

- Compute the Disparate Impact Ratio (minority rate/majority rate)

- Head over to further analysis if the ratio drops below 0.8 (the 80% rule)

A real-life example shows why this testing matters. A fintech startup found that their credit-scoring model denied loans to Black applicants at a rate 30% higher than white applicants with similar profiles. They cut this gap to 5% by using counterfactual analysis and removing proxy variables like ZIP codes. This met both their internal policies and regulatory requirements.

Financial institutions should also add these advanced approaches:

- Causal modeling helps find subtle biases that statistics might miss

- Representative algorithmic testing measures fairness in a variety of populations

- Open-source toolkits like IBM AI Fairness 360, Aequitas, and Google What-if help measure discrimination and test solutions

Fair Lending Compliance Under ECOA and UDAAP

ECOA bans lenders from discriminating based on race, gender, or other protected characteristics. ECOA rules cover all credit decisions—even those from complex algorithms.

The CFPB now includes discriminatory conduct in its definition of “unfair” within UDAAP. The Bureau also plans to check “models, algorithms and decision-making processes” used in consumer financial services.

These practices help maintain compliance:

- Test all AI models yearly for fair lending, plus extra tests after updates

- Run periodic matched pairs testing to spot different outcomes for similar applicants

- Watch weighted variables that might unfairly affect protected groups

- Look for and use less discriminatory alternatives (LDAs) when finding unfair impacts

Federal enforcement might have eased on disparate impact, but ignoring it creates huge legal and reputation risks. The Massachusetts Attorney General’s $2.50 million settlement with a student loan company in 2025 shows state authorities still watch AI discrimination closely. Clearly, complete bias testing protects against heavy financial penalties and reputation damage.

Proven Way #5: Strengthen AI Data Governance Practices

Strong ai data governance forms the foundations of preventing model risk penalties. AI systems in financial services keep evolving. The way organizations handle their data now determines both compliance outcomes and model performance.

Data Lineage and Consent Management

Data lineage tracking builds trust in reports and data. This helps financial institutions respond quickly during regulatory investigations. Organizations that use automated lineage have seen improved productivity by up to 40%. They can trace data-related problems to their source 90% faster than manual methods. Financial organizations need transparent consent management practices. These practices should respect user privacy and ensure AI systems work properly.

AI-powered financial services need explicit consent. This becomes vital when you profile users or make automated decisions that affect them. The CFPB states financial institutions can’t use “black-box” technology that hides specific reasons behind adverse actions. Breaking these rules leads to heavy penalties. Companies face fines up to $100,000 per violation while board directors could pay $10,000.

Minimizing Use of Sensitive or Proxy Variables

Financial institutions don’t deal very well with proxy discrimination. Algorithms often use neutral-looking variables that associate with protected characteristics like race. To name just one example, see how mobile application location data can hint at zip codes, which often link to race. This creates major regulatory risks, especially since many states now restrict variables that might cause unfair discrimination.

Organizations need these steps to minimize data effectively:

- Identify and map all ML processes where personal data might be used

- Assess which features matter most to your purpose

- Use standard feature selection methods to keep only needed variables

- Avoid collecting personal data just because it might help later

Cross-Border Data Transfer Compliance

Fintech companies handling data transfers between countries face complex rules. The GDPR sets strict conditions on personal data moving outside the European Economic Area. Data protection must match European standards. Companies can comply through adequacy decisions, Standard Contractual Clauses (SCCs), and Binding Corporate Rules (BCRs).

Technical solutions help manage cross-border compliance. Regional data storage satisfies data residency requirements. Data classification frameworks sort information by sensitivity. Advanced methods like federated learning enable teamwork without moving raw data. These approaches keep companies compliant while their AI systems run smoothly.

Proven Way #6: Document Everything for Audit Readiness

Documentation forms the foundation of defensible ai governance. Your financial institution can avoid expensive penalties and handle regulatory reviews better with proper documentation. Detailed documentation shows how AI systems work, make decisions, and what risks they might have.

Model Development and Assumption Logs

Model Development Documents (MDDs) help validators check regulatory compliance effectively. A good MDD should include:

- Data sources and preprocessing steps

- Model architecture and training processes

- Performance metrics and testing methodologies

- The model’s assumptions and limitations

Your team needs specific people to handle MDDs. This creates clear ownership and keeps documentation quality high even when team members change.

Change Management and Version

Git and similar version control systems help track changes throughout the model’s life. You need complete information for each deployment. This includes the dataset used, chosen hyperparameters, approval details, and validation metrics applied.

Financial institutions should create AI action plans that cover governance frameworks, cybersecurity risk management, and documentation needs. This integrated approach lets organizations back up every AI-generated estimate with clear proof.

Want to improve your documentation methods? Book a Readiness Call to learn how strong documentation protocols can shield your organization from regulatory penalties while getting the most from AI.

Key Takeaways

Financial institutions can avoid costly AI model risk penalties by implementing six proven governance strategies that balance innovation with regulatory compliance.

• Build contextual AI governance frameworks that align with your business objectives rather than imposing generic restrictions that stifle innovation.

• Implement robust model risk management controls including SR 11-7 compliance, continuous performance monitoring, and systematic drift detection.

• Ensure explainability using SHAP and LIME tools to provide specific adverse action notices and avoid the rejected “black box” defense.

• Conduct regular bias audits across protected classes using disparate impact testing to maintain ECOA and UDAAP compliance.

• Strengthen data governance practices through comprehensive lineage tracking, consent management, and minimizing proxy variables that could cause discrimination.

• Document everything for audit readiness with detailed model development logs, version control systems, and complete change management processes.

The regulatory landscape has permanently shifted—AI systems receive no special treatment under consumer protection laws, and “the algorithm decided” is no longer a legally defensible explanation. Organizations that proactively implement these governance practices will not only avoid million-dollar penalties but also build sustainable competitive advantages through responsible AI deployment.

FAQs

Q1. What are the key components of an effective AI governance framework for financial institutions? An effective AI governance framework typically includes clear definitions, a comprehensive inventory of AI systems, detailed policies and standards, and robust controls for monitoring and validation. It should align with business objectives and reflect the organization’s specific operational realities.

Q2. How can financial institutions ensure their AI models comply with fair lending regulations? Financial institutions can ensure compliance by conducting regular bias and fairness audits, performing disparate impact testing across protected classes, and implementing strong data governance practices. They should also provide specific, accurate reasons for adverse credit decisions and avoid using “black box” defenses.

Q3. What are some best practices for model risk management in AI-powered financial systems? Best practices include implementing comprehensive model validation and performance monitoring, establishing clear retraining triggers to address model drift, and ensuring compliance with regulatory standards like SR 11-7. Regular testing and documentation of model assumptions and limitations are also crucial.

Q4. How can fintech companies address the challenges of cross-border data transfers in AI systems? Fintech companies can address cross-border data transfer challenges by implementing regional data storage, developing data classification frameworks, and utilizing advanced techniques like federated learning. They should also ensure compliance with regulations like GDPR through mechanisms such as adequacy decisions and Standard Contractual Clauses.

Q5. Why is thorough documentation important for AI governance in financial services? Thorough documentation is critical for audit readiness and regulatory compliance. It provides transparency into AI systems’ capabilities, decision-making processes, and potential risks. Comprehensive documentation, including model development logs and version control, helps financial institutions justify AI-generated decisions and withstand regulatory scrutiny.